The Italian road transport sector continues to go through a difficult period, caught between the slowdown in growth on a macroeconomic level, competition with foreign carriers and the need to renew its business model, to respond to the challenges imposed by the market and technological evolution.

The Contship Italia Group has always been committed to develop and provide the market with intelligent intermodal solutions, capable of combining the efficiency and sustainability of rail transport with the flexibility of road transport. The underlying assumption is that a long distance transport model based on the exclusive use of trucks is no longer sustainable, neither from the environmental point of view, the economic and social point of view, nor the operational perspective, in particular when it is adopted to transport large volumes and serve large size producers and distributors, who are becoming increasingly attentive to the impact and organization of their supply chain.

The evolution of the competitive environment and the growing expectations regarding the respect of the environment and the work conditions impose, our opinion, an evolution of the road transport business model. This evolution requires a new approach, considering all the externalities generated by the various modes of transport, to drive customers, operators and political decision makers towards far-sighted strategic choices.

For this reason, we choose to contribute to the debate by developing a White Paper, dedicated to the main challenges faced by the Italian road haulage sector; here we put together data and considerations that we hope might be valuable to all the decision makers in the field.

The Italian situation

Road haulage represents by far the most used transport modality for freight transport; in Italy, more than 85% of all transport, in terms of tonne-kilometer, is performed by truck. The average distance of national transports is about 115 km, while international transports involving Italian trucking companies are on average longer than 600 km.

On both a national and international level, Italian trucking companies suffer from the competition with foreign operators; on one side, there is the problem of the commoditization of the transport activity, which is often seen as a mere cost, to be compressed as much as possible; on the other side, the constant increase of operational costs continues to erode operational margins and to reduce the competitiveness of Italian operators.

The majority of international transport activities involving Italy crosses the Alps at the borders with Austria, France and Switzerland. The modal split on these routes reflects the infrastructural differences and the strategic choices implemented by the three Countries: in France, road haulage accounts for almost all volumes (92% moving on the road, against less than 8% moving by train); in Austria road haulage is still dominant, but the use of rail increases (30% of volumes moving by train); Switzerland is best in class, with more than 70% of volumes transported by rail.

The shortage of qualified drivers

One of the most pressing problems for the sector, which also involves countries such as Italy, which are experiencing a generalised decline in turnover, is the lack of qualified drivers. According to a report by the German association DSLV, two thirds of drivers in Germany will retire in the next 15 years and there is already a shortage of around 45,000 drivers, due to the fact that 30,000 operators leave the profession every year, whilst only 2,000 people obtain, in the same period, a professional qualification for driving heavy vehicles. The situation is equally severe in France, with a shortage of about 20,000 drivers and in Italy, where the estimates of industry associations speak of at least 15,000 missing drivers.

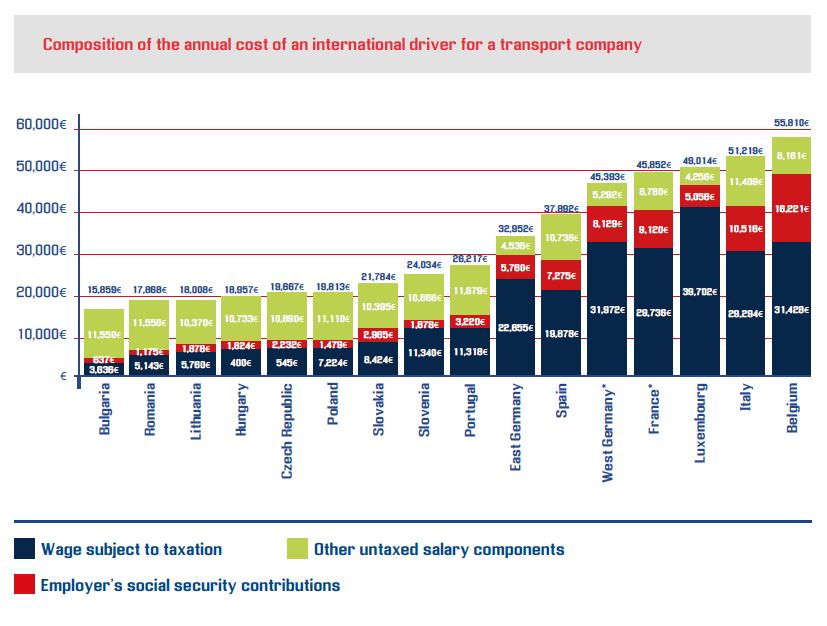

Cost of labour and operating costs of heavy vehicles

As far as labour costs are concerned, substantial differences between the various countries persist; Italy is the second country, after Belgium, where labour costs are higher, more than twice as high as in countries such as Bulgaria, Romania, Lithuania, Hungary, the Czech Republic, Poland, Slovakia and Slovenia.

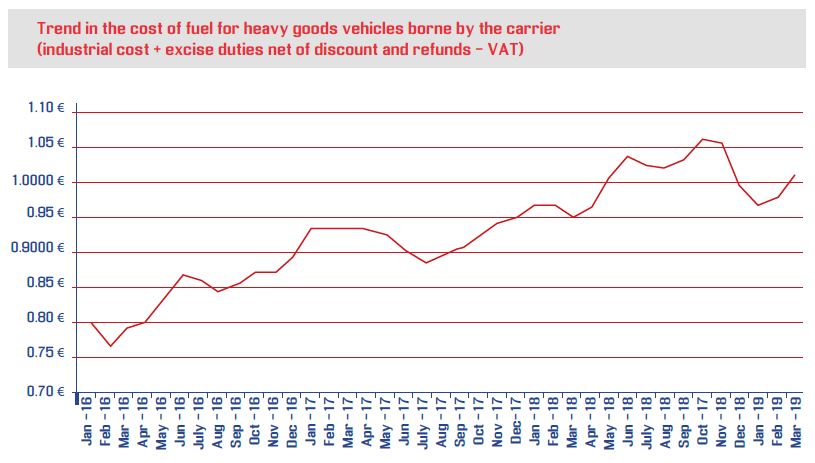

This graphic shows a summary of the main operating costs of a road train. The average operating cost per kilometre is obtained comparing the total costs (excluding structural costs) to the average distance, estimated at 115,000 km/year. (source: Hannibal S.p.A.)

The cost of fuel, in order of importance, represents a further element of compression of operators' margins, also in virtue of the price increases recorded in recent years (+26% from January 2016 to March 2019).

The challenge of change

If one analyses the data collected, it is clear that the sustainability of the traditional business model of long-distance road transport is threatened on several fronts. The room for manoeuvre is becoming increasingly narrow and many of the classic cost-containment strategies (wage compression and the use of low-cost labour, social dumping and lengthening of the life cycle of vehicles) are no longer feasible, even in light of new, stringent regulations and a general evolution of sensitivity in this area.

From problems to solutions

The crux of the matter remains the need to redistribute heavy goods traffic, limiting long-distance journeys as much as possible and exploiting the flexibility of the road carrier to effectively serve first and last-mile distribution, whilst at the same time improving the availability, speed and quality of intermodal rail services, which already currently represent a reliable and sustainable alternative to all-road transport, on the leading national and international routes.

To make this modal shift possible, it is necessary to take inspiration from the realities that have successfully undertaken this path, obtaining concrete results. This is the case of Switzerland, which in the last 25 years has shifted a significant share of freight traffic from road to rail, thanks to a combination of innovative policies and funding that encourage and facilitate the conversion, reaching in 2018 an enviable ratio 72/28 between rail and road, for transalpine freight traffic.

the role of public opinion, corporate social responsibility and policy-makers

The growing attention to sustainability issues understood not only as attention to environmental issues but as a long-term approach to economic and social development, requires an acceleration of the change taking place, also in other European countries. As highlighted at the beginning of this report, the transport sector is responsible for a share of emissions and negative externalities, but is at the same time, one of the pillars of economic development, and a vital element of the trading economy, which ensures prosperity and development to the entire European continent. For this reason, the challenge of developing the system must be seen as an indispensable, concrete opportunity within the reach of governments, operators and the most far-sighted carriers.

For national and EU policy-makers, it is essential to open a constructive dialogue with the world of industry, representatives of road haulage companies and the world of logistics, with particular attention to the demands of intermodal operators, which are already currently engaged in the commercial development of railway alternatives. Politicians have the task of stimulating a genuine and factual debate on the need to pursue substantial infrastructure development; at the same time, the right incentives must be introduced to direct investment towards the most sustainable modes of transport, making solutions that reduce road congestion, pollution and the negative externalities of road abuse increasingly competitive.

Hauliers have a responsibility to assess, with due foresight, the sustainability of the transport model proposed to the market, rejecting practices such as social dumping and cutting costs related to the safety of operations and proper management of the fleet and staff. Overcoming only downward competition, specialising in serving niche markets sensitive to innovation, energy efficiency and service quality, can be a winning strategy to ensure growth in the medium and long term. In doing so, however, companies cannot be left alone: it is necessary to support them by developing - amongst customers and end consumers - a greater awareness of the risks associated with excessive compromises linked to the search for the lowest possible price, the expectation of ever-faster deliveries and "zero cost".

To learn more and take part in the discussion, we invite you to download and share the White Paper “Italian road haulage in the midst of the economic crisis, international competition and new business models”: